Credit Spring – Understanding the Unique Loan Membership Model and How It Works

Credit Spring is a UK-based financial service provider that operates with a distinctive approach to lending. Instead of functioning as a traditional lender that issues loans with interest and complex repayment terms, Credit Spring uses a membership-based model. This means that customers pay a fixed monthly fee to gain access to short-term credit when needed, without paying interest on the borrowed amount.

The service is designed for people who may not have an extensive credit history or who find it difficult to access conventional credit options. It aims to provide financial safety nets for unexpected expenses, ensuring that members avoid high-cost credit traps like payday loans.

How the Credit Spring Membership Work

At its core, the Credit Spring concept is quite simple:

- You choose a membership plan.

- You pay a fixed monthly subscription fee.

- You get access to a set amount of credit per year, split into instalments.

- You repay the borrowed sum in equal monthly instalments, with no interest charges.

The key difference is that instead of paying interest each time you borrow, you’re paying for the access to credit in advance via the subscription fee. This removes the uncertainty of fluctuating interest rates and hidden costs, giving members predictable borrowing costs.

Credit Spring Membership Plans

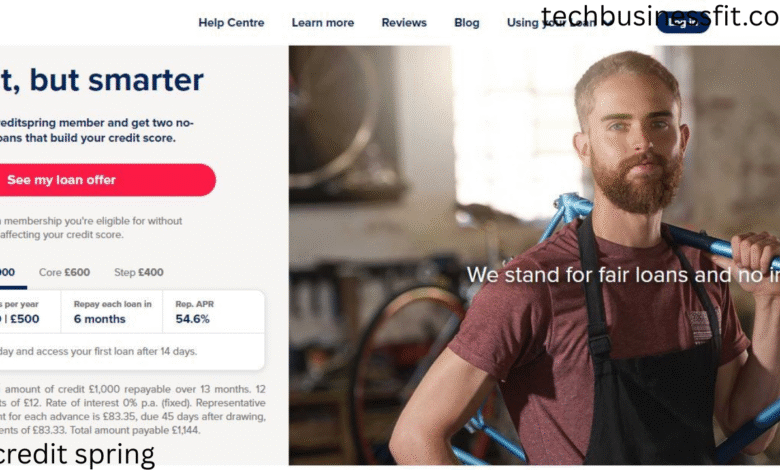

Credit Spring offers several membership tiers, each designed for different borrowing needs:

- Core Plan:

- Typically offers two instalments of around £250 each per year.

- Fixed monthly membership fee.

- Interest-free borrowing with a set repayment period.

- Plus Plan:

- Provides two instalments of a larger amount, often £500 each per year.

- Slightly higher monthly subscription fee.

- Same interest-free policy.

These plans are tailored to ensure members only borrow what they can realistically repay, helping them manage their finances without falling into a debt spiral.

Eligibility and Application Process

Applying for Credit Spring membership involves:

- Filling out a short online application.

- Passing an affordability check rather than a purely credit-score-based assessment.

- Providing bank account details for direct debit payments.

Unlike many lenders, Credit Spring focuses on whether you can afford the monthly subscription and repayments, rather than purely relying on your credit history. This makes it more accessible for people with lower or limited credit scores.

Benefits of Credit Spring

Predictable Costs

Because you pay a fixed subscription fee each month, you know exactly how much borrowing will cost over the year. There are no hidden charges, late payment penalties, or variable interest rates.

No Interest Charges

One of Credit Spring’s biggest advantages is that loans are interest-free. The only cost is your membership fee, which remains the same regardless of how much you borrow within your plan limits.

Credit Score Building

Credit Spring reports to credit reference agencies. Making repayments on time can help improve your credit history and make it easier to access other forms of credit in the future.

Access to Emergency Funds

Members can request their instalments whenever they face unexpected expenses — such as car repairs, home emergencies, or urgent bills — without having to go through a lengthy loan approval process.

Financial Education Tools

Some memberships also include budgeting tools, credit score tracking, and financial health tips to help members improve their overall money management.

Drawbacks and Considerations

Membership Fee Regardless of Usage

Even if you don’t borrow any money, you still have to pay the monthly membership fee. This means you must weigh the cost against the likelihood of needing the credit during the year.

Limited Loan Amounts

Credit Spring is designed for small, short-term borrowing. If you need larger sums, this may not be the best option for you.

Fixed Repayment Schedules

While predictability is a benefit, it also means you must stick to a set repayment plan, which might not be flexible if your income fluctuates.

UK-Only Service

Credit Spring operates solely in the UK, meaning it’s not an option for borrowers in other countries.

Who is Credit Spring Best For?

Credit Spring is particularly suited for:

- People with fair or limited credit history.

- Those who want a safety net for emergencies without paying high interest rates.

- Individuals who appreciate predictable costs and straightforward repayment schedules.

- Borrowers who want to improve their credit profile through consistent repayments.

It is less ideal for:

- People who rarely borrow money and wouldn’t benefit from the membership.

- Those needing large or long-term loans.

Comparison with Traditional Loans

| Feature | Credit Spring | Traditional Loan |

|---|---|---|

| Interest Charges | No | Yes |

| Costs | Fixed monthly fee | Varies by lender/interest rate |

| Credit Requirements | More flexible affordability checks | Often stricter credit score requirements |

| Repayment Structure | Fixed monthly instalments | May vary, sometimes flexible |

| Borrowing Limits | Small, short-term amounts | Larger sums possible |

Credit Spring stands out by removing the interest component, but it limits the borrowing size to keep debt manageable.

How Credit Spring Helps Build Financial Stability

By offering a clear and predictable cost structure, Credit Spring helps members avoid the uncertainty of traditional credit products. Timely repayments are reported to credit bureaus, potentially boosting credit scores. Additionally, the educational resources provided can improve members’ financial habits over time.

This approach is especially beneficial for individuals who have previously struggled with managing debt or have been rejected by traditional lenders. By creating a controlled borrowing environment, Credit Spring aims to break the cycle of high-interest debt traps.

Final Thoughts on Credit Spring

Credit Spring is not just another lending company — it’s a membership-based credit service designed to provide financial breathing space for its members. While it’s not suitable for everyone, it can be a valuable tool for those needing small, short-term loans without the burden of interest rates.

Its transparent fee structure, accessibility, and potential to improve credit scores make it an attractive alternative to payday loans and high-cost credit cards. However, the key to benefiting from Credit Spring lies in assessing your borrowing habits and ensuring that the subscription cost justifies the potential borrowing you might require.

By understanding its model, benefits, and limitations, borrowers can make informed decisions about whether Credit Spring is the right financial safety net for them.

also read: Scottish Widows, ??, and a Legacy of Financial Protection